Simple Mortgage Calculator: This calculator shows your monthly payment on a mortgage; with links to articles for more information.

Mortgage Calculator

How to calculate your mortgage payments

Here’s how to use our mortgage calculator to easily estimate payments:

- Enter your Principal Amount:. In the Principal Amount: field, input the amount.

- Enter your Annual Interest Rate. In the Annual Interest Rate field, input the rate you expect to pay or are currently paying.

- Enter your Number of Years In the Number of Years field, enter the length of your loan.

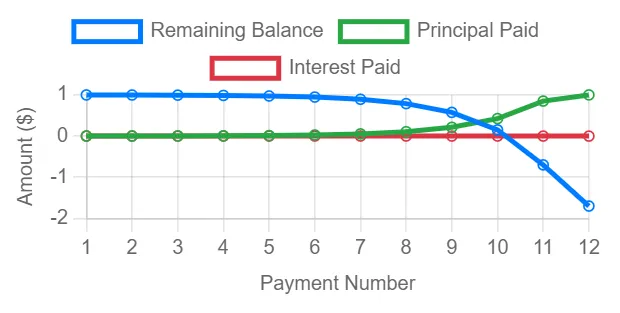

–

Table of Contents

How to easily calculate mortgage payment?

Calculating your mortgage payment doesn’t have to be a daunting task. By breaking it down into simple steps, you can easily determine how much you’ll need to pay each month.

Start by gathering key information such as the loan amount, interest rate, and term of the loan. Use an online mortgage calculator or the basic formula (PMT = P[r(1+r)^n]/[(1+r)^n-1]) to crunch the numbers swiftly.

Remember that there are additional costs to consider besides just the principal and interest. Property taxes, homeowner’s insurance, and private mortgage insurance (if applicable) will all contribute to your overall housing costs.

By factoring in these expenses upfront, you’ll get a more accurate picture of what your monthly payments will look like.

Don’t be intimidated by the complexities of mortgage calculations; with a bit of guidance and attention to detail, you can navigate this process with confidence.

How do you calculate simple interest on a mortgage?

When it comes to calculating simple interest on a mortgage, the process is quite straightforward yet essential for understanding how much you’ll end up paying over time.

To calculate simple interest on a mortgage, you first need to know the principal amount borrowed (the initial loan amount), the annual interest rate charged by the lender, and the length of time you will be repaying the loan.

By multiplying the principal amount by the annual interest rate and then multiplying that result by the number of years or months of repayment, you can determine how much interest will accrue over time.

Understanding this calculation can give borrowers valuable insights into their total repayment costs and help them make informed decisions when choosing a mortgage product.

Additionally, it’s crucial to note that while simple interest calculations are helpful in determining an approximate loan cost, they may not provide an exact representation of what borrowers will pay due to additional factors like taxes or insurance.

Being aware of these nuances can empower individuals to ask relevant questions when discussing mortgage terms with lenders and ensure they have a comprehensive understanding of all associated costs.

Ultimately, by grasping how simple interest impacts their mortgage obligations, borrowers can take control of their financial decisions and plan more effectively for their future homeownership journey.

How much is a 500 000 mortgage payment?

When taking out a 500,000 mortgage, the monthly payment amount can vary based on several factors such as interest rate, loan term, and type of mortgage.

For example, with a 30-year fixed-rate mortgage at a 4% interest rate, your monthly payment might be around $2,387.08 excluding insurance and taxes.

Opting for a shorter loan term or a different interest rate could significantly impact the final payment amount.

Understanding the breakdown of your mortgage payments is crucial in managing your finances effectively. It’s important to also consider additional costs like property taxes, homeowners insurance, and private mortgage insurance (PMI) that may affect the overall expense.

By utilizing online mortgage calculators or consulting with financial advisors, potential homeowners can gain insights into creating a feasible budget plan that accommodates their monthly payments without straining their pockets.

By exploring various scenarios and being aware of all associated expenses that come with borrowing such a significant sum like $500,000 for a home purchase, individuals can make informed decisions about affordability and financial planning for long-term commitment.

The key is to stay educated on market trends and seek guidance from professionals when navigating through complex mortgage processes to ensure financial stability in the long run.

What is the formula for home mortgage?

When it comes to understanding home mortgages, one key aspect is knowing the formula that determines monthly mortgage payments.

The formula for calculating a home mortgage payment involves several variables, including the loan amount, interest rate, and loan term.

By plugging these values into the formula, borrowers can estimate their monthly payment.

To calculate your monthly mortgage payment, you can use the following formula: M = P[r(1+r)^n]/[(1+r)^n-1].

In this equation, M represents the total monthly mortgage payment, P is the principal loan amount, r is the monthly interest rate (annual rate divided by 12), and n is the number of months in the loan term.

By understanding this formula and how each variable affects your payment amount, you can better plan for your future homeownership.

Moreover, it’s essential to consider other factors such as property taxes and homeowners insurance when budgeting for a mortgage.

While the formula provides a basic calculation of your monthly payment amount based on principal and interest components, additional expenses should not be overlooked.

Understanding the complete picture of homeownership costs will help you make informed decisions about purchasing a home within your financial means.

Simple mortgage calculator formula

Understanding the simple mortgage calculator formula is crucial for anyone considering taking out a home loan. This formula typically involves three main components: the principal amount borrowed, the annual interest rate, and the loan term in years.

By plugging these values into the formula, borrowers can quickly determine their monthly mortgage payment.

Additionally, it’s important to consider other factors that may affect your mortgage calculations, such as property taxes, home insurance, and private mortgage insurance (PMI).

These additional costs can significantly impact your overall monthly payments and should not be overlooked when using a simple mortgage calculator.

By incorporating these variables into your calculations, you can gain a more accurate picture of what your total monthly housing expenses will look like.

In conclusion, while the simple mortgage calculator formula provides a basic estimate of your monthly payments, it’s essential to remember that there are various factors at play in determining the true cost of homeownership.

Being aware of all these elements and utilizing them in conjunction with the basic formula can help you make informed decisions when it comes to getting a mortgage.

Google mortgage calculator

Considering the complexities of mortgage calculations, Google Mortgage Calculator stands out as a user-friendly tool that simplifies the process for home buyers.

With just a few inputs like loan amount, interest rate, and term length, users can quickly estimate their monthly payments and total interest paid.

This tool provides valuable insights into different loan options and allows individuals to make informed decisions regarding their home purchase.

Furthermore, Google Mortgage Calculator offers a straightforward interface that is accessible on both desktop and mobile devices. This convenience allows users to perform quick calculations on the go or during property visits.

By utilizing this tool, potential home buyers can adjust variables such as down payment amounts or interest rates to see how they impact their overall mortgage terms.

Ultimately, Google Mortgage Calculator empowers consumers with essential financial information to guide them through the home buying process effectively.

free mortgage calculator

When it comes to navigating the complex world of mortgages, having a reliable tool at your disposal can make all the difference.

A free mortgage calculator is like a financial Swiss army knife that empowers you to explore different scenarios, compare rates, and determine the best path forward in your home-buying journey.

By simply inputting variables such as loan amount, interest rate, and term length, you can quickly generate accurate estimates of your monthly payments and total interest over time.

Moreover, a free mortgage calculator offers more than just basic number crunching – it provides invaluable insights into how different factors influence your overall loan dynamics.

Whether you’re considering refinancing options or assessing the impact of making additional payments towards your principal balance, this tool allows you to visualize various scenarios and tailor your financial strategy accordingly.

Ultimately, by leveraging the capabilities of a free mortgage calculator, you gain clarity and confidence in making informed decisions that align with your long-term goals.

Mortgage payment calculator

When it comes to managing your finances and planning for the future, having a reliable mortgage payment calculator can be a game-changer.

This tool not only helps you estimate your monthly payments but also allows you to explore different scenarios and make informed decisions about your mortgage.

By inputting variables such as loan amount, interest rate, and term length, you can quickly see how these factors impact your overall payment structure.

Moreover, a mortgage payment calculator can provide valuable insights into the potential cost savings of making extra payments towards your principal balance.

By adjusting parameters within the calculator, you can visualize how additional payments could shorten the term of your loan and ultimately save you money on interest in the long run.

This level of transparency empowers borrowers to take control of their financial situation and work towards achieving their homeownership goals sooner than anticipated.

Mortgage calculator USA

Mortgage calculators have significantly simplified the process of understanding loan repayments in the USA. These online tools offer users the ability to input variables such as loan amount, interest rate, and term length to calculate estimated monthly payments.

This level of transparency empowers borrowers to make informed decisions when exploring different mortgage options.

Moreover, with the rising popularity of adjustable-rate mortgages (ARMs) in the USA, mortgage calculators play a crucial role in helping individuals assess potential changes in their monthly payments over time.

By simulating different scenarios and comparing various loan products, users can better understand how fluctuations in interest rates may impact their financial commitments.

Ultimately, utilizing a mortgage calculator can provide peace of mind and clarity during the home buying process by offering a clear snapshot of what to expect financially throughout the life of a loan.

Simple mortgage calculator formula excel

Calculating mortgage payments can be a daunting task for many individuals, but with the use of an Excel spreadsheet and a simple formula, this process can become much more manageable.

By utilizing Excel’s functions, such as PMT and IPMT, one can easily determine their monthly mortgage payment amount and track the allocation of each payment towards interest and principal.

This level of transparency empowers individuals to make informed decisions about their finances and plan ahead effectively.

Moreover, customizing the Excel spreadsheet to include additional features like extra payments or varying interest rates can provide users with a comprehensive view of their mortgage obligations over time.

This interactive approach not only helps in understanding the financial implications of different scenarios but also encourages borrowers to strategize on how they can pay off their mortgages faster or save on interest costs.

Ultimately, by leveraging the simplicity and versatility of Excel in calculating mortgage details, individuals gain control over their financial well-being and are better equipped to manage one of life’s significant investments – homeownership.

Monthly payment calculator

Calculating your monthly mortgage payments can be a crucial step in understanding the financial commitment of buying a home.

With the help of a reliable monthly payment calculator, you can easily estimate how much you’ll need to budget each month towards your mortgage.

This tool provides a clear breakdown of principal and interest payments, giving you the insight needed to make informed financial decisions.

By inputting variables such as loan amount, interest rate, and term length into a monthly payment calculator, you gain a deeper understanding of how these factors impact your overall financial obligations.

Moreover, these calculators often come equipped with additional features like property tax estimations and insurance costs, providing an all-encompassing view of what your total expenses may look like.

Armed with this knowledge, you can confidently plan for homeownership with more clarity and foresight.

Understanding the importance of using a monthly payment calculator empowers individuals to navigate the complexities of homeownership more effectively.

By taking advantage of this user-friendly tool, potential homebuyers can tailor their financial strategies to align with their specific needs and goals.

Ultimately, utilizing a monthly payment calculator removes uncertainty from the equation and allows for better preparation when entering into one of life’s major investments—a new home purchase.

Simple mortgage calculator with down payment

Calculating your mortgage payments can sometimes feel like navigating a maze of numbers and percentages. However, introducing a down payment into the equation can simplify the process significantly.

By using a simple mortgage calculator with a down payment feature, homebuyers can see firsthand how adjusting this initial cash outlay affects their monthly installments and overall loan amount.

This tool allows for better financial planning and helps individuals understand the impact of different down payment amounts on their long-term budget.

Moreover, incorporating a down payment into your calculations can provide insights into potential savings on interest over the life of the loan.

Even a modest increase in your initial deposit can lead to substantial reductions in interest payments, ultimately saving you thousands of dollars over time.

Additionally, using a mortgage calculator that factors in down payments enables buyers to set realistic goals and tailor their housing budget according to their financial capabilities – making the homeownership journey more manageable and empowering.

Conclusion

In conclusion, using a simple mortgage calculator can be an incredibly useful tool for anyone looking to buy a home.

It provides a quick and easy way to estimate monthly payments and determine affordability based on different loan terms.

By inputting key information such as the loan amount, interest rate, and term length, users can gain valuable insights into their financial commitments.

While the results may not be exact due to factors like taxes and insurance, they offer a helpful starting point for planning your budget. So next time you’re considering a mortgage, give a simple mortgage calculator a try and take control of your homebuying journey today.